Domino's (DPZ) Faces Skepticism Amid Sluggish Growth and Questionable Valuation

Domino's (DPZ) underperforms despite beating revenue estimates, as analysts question its growth potential amid stagnant demand and a 20.7x valuation.

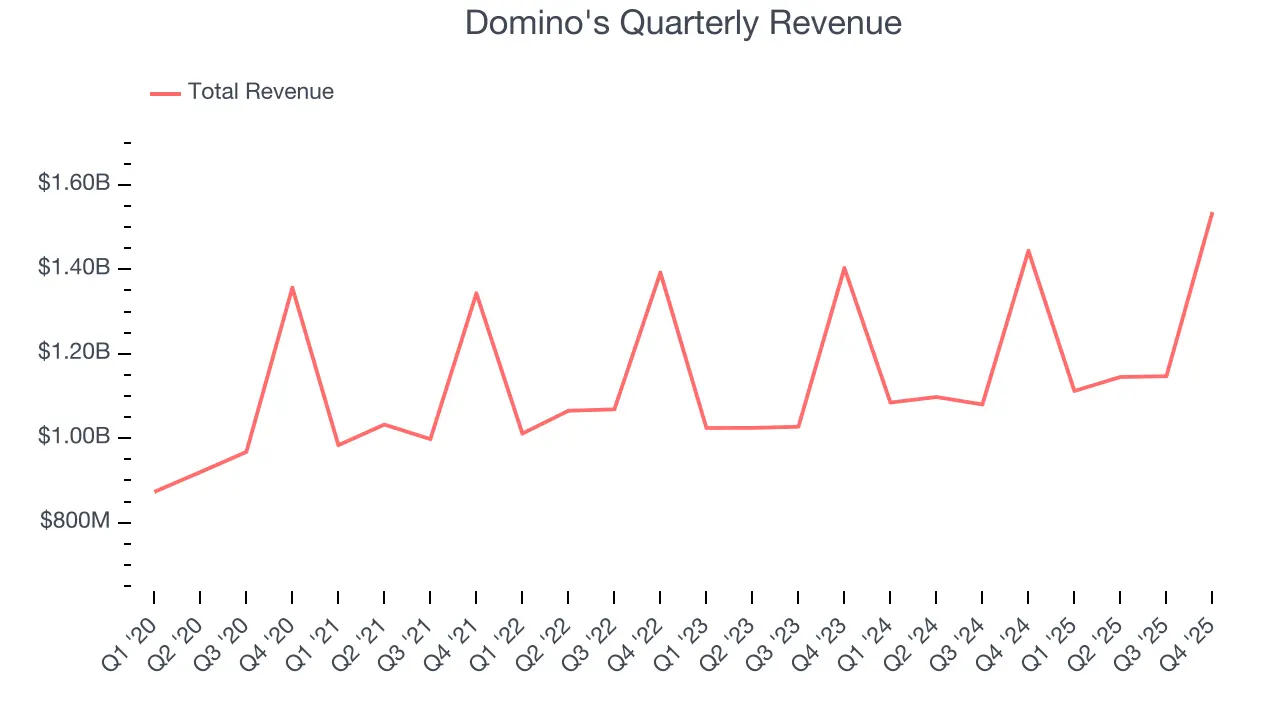

The pizza chain reported Q4 CY2025 revenue of $1.54 billion, a 6.4% YoY increase that outpaced estimates by 1.2%. However, GAAP EPS of $5.35 fell 0.7% below expectations, and the stock trades at a forward P/E of 20.7x—well above peers like Yum! Brands (YUM) and McDonald's (MCD).

The disconnect lies in three key metrics. First, Domino's historical revenue growth of 5.3% annually over six years lags behind its 5.9% forward guidance, raising questions about the durability of its expansion.

Second, while earnings per share (EPS) have grown at a 10.7% CAGR, revenue growth remains significantly lower, signaling margin compression risks. Third, the 20.7x forward P/E ratio suggests investors are paying a premium for incremental growth, despite a net-debt-to-EBITDA ratio of 4.5x that analysts call "safe".

Same-store sales rose 3.7% YoY, up from 1.6% in the prior-year quarter, and store count grew 3.5% to 22,142 locations. Free cash flow margin expanded to 11.5% in Q4, up from 9.4% YoY, but the market remains unconvinced.

With a current price of $400.50 versus a $482.97 Wall Street price target, the stock reflects skepticism about its ability to sustain momentum.

Look, the math doesn’t lie: when EPS growth outpaces revenue growth, investors start asking if margins are masking underlying demand issues. Domino’s has the numbers to satisfy short-term bulls, but the valuation math suggests the market is pricing in a future that may not materialize.

⚠️ LEGAL DISCLAIMER: This article is for informational purposes only and does not constitute financial or investment advice.